In this brief article, we share the Six-Point Plan that can guide you toward a successful retirement.

With the significant changes in economic and financial market conditions, having a sound plan is more important than ever so you can stay in control of and on track towards your ideal retirement. As a society, and personally, we are confronted with the challenges of rising inflation and interest rates, falling share and property prices, and a worsening geopolitical backdrop.

The Six-Point Plan outlined below is designed to help you think clearly through the current financial noise and arrive at your retirement destination with minimal turbulence.

1. Articulate, set, and put numbers and timelines on all goals

Fully identifying goals is the essential first step toward building a retirement portfolio structure. Many people only think of a couple of goals, such as the amount of annual cash flow required to live or the amount of capital needed for annual travel, but a deep dive into your goals and objectives should include all desired future spending, including but not limited to:

• annual cash flows for recurring expenses, both necessary and discretionary;

• family needs (specific financial help to parents, children, or grandchildren);

• capital spending to maintain or upgrade lifestyle assets (such as homes, cars, or boats);

• aged care funding;

• estate planning and bequests;

• longevity funding (so your money doesn’t run out before you do); and

• philanthropy.

2. Build a financial model to assess the amount of money you need to meet future goals, and refine your goals and timelines as required

According to the 2020 Retirement Income Review Report, people often have the financial capacity to retire earlier, spend more money themselves (or help others), and enjoy life more fully than they actually do.

Why? Because they lack the means to accurately understand their financial capacity; therefore, they take an overly cautious approach to living throughout retirement. Not that people should be overly optimistic, but professional financial modelling as part of a broader retirement plan can reveal whether goals are likely to be met or not, and therefore allow people to proceed with confidence or adjust as necessary. Based on personal goals, financial modelling can answer the question ‘do I have enough money to retire?’.

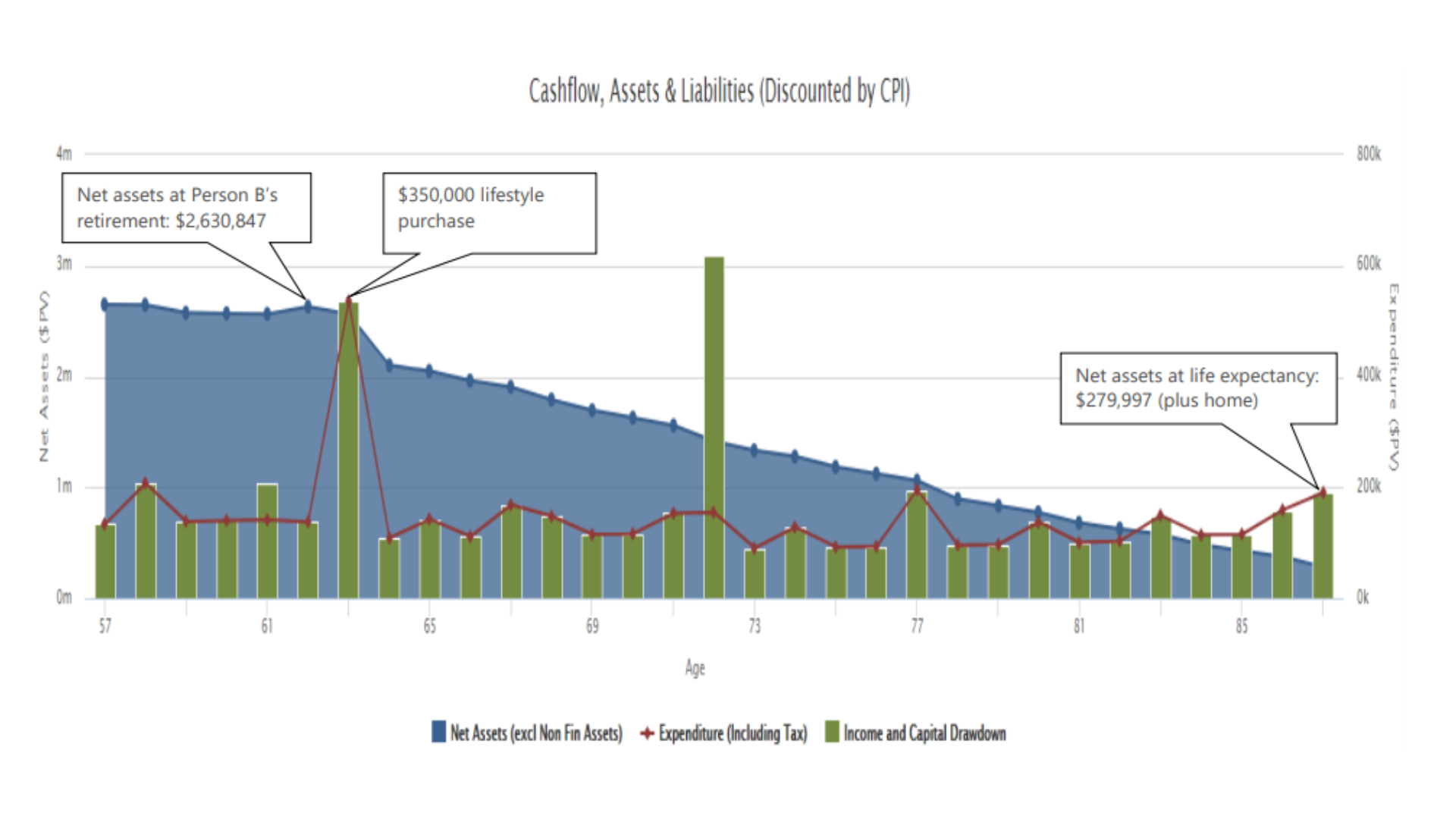

See our whitepaper, Predicting the Future 2023+, for an in-depth review of the benefits of personal financial modelling. Below, we have shared a financial modelling output example.

Figure 1: An example of a financial modelling output

3. Implement strategies and utilise optimal investment structures (such as superannuation funds, family trusts, and/ or companies) to minimise tax and achieve asset protection

For people with high incomes and/ or high net worth, tax planning and utilising optimal investment structures is essential. All structures in Australia have pros and cons, but they tend to be used because they can provide the twin benefits of reducing tax and affording asset protection. What may be the best mix of financial strategy and structure is often very personal and subject to age, family situation, and level of wealth. Getting tax planning right and allocating capital to the right structures can make a huge difference to your retirement success. Once you settle on where the money should be, you can then undertake estate planning with more certainty.

The importance of making the right financial decisions based on your circumstances is explored in our whitepaper, Event-Based Advice.

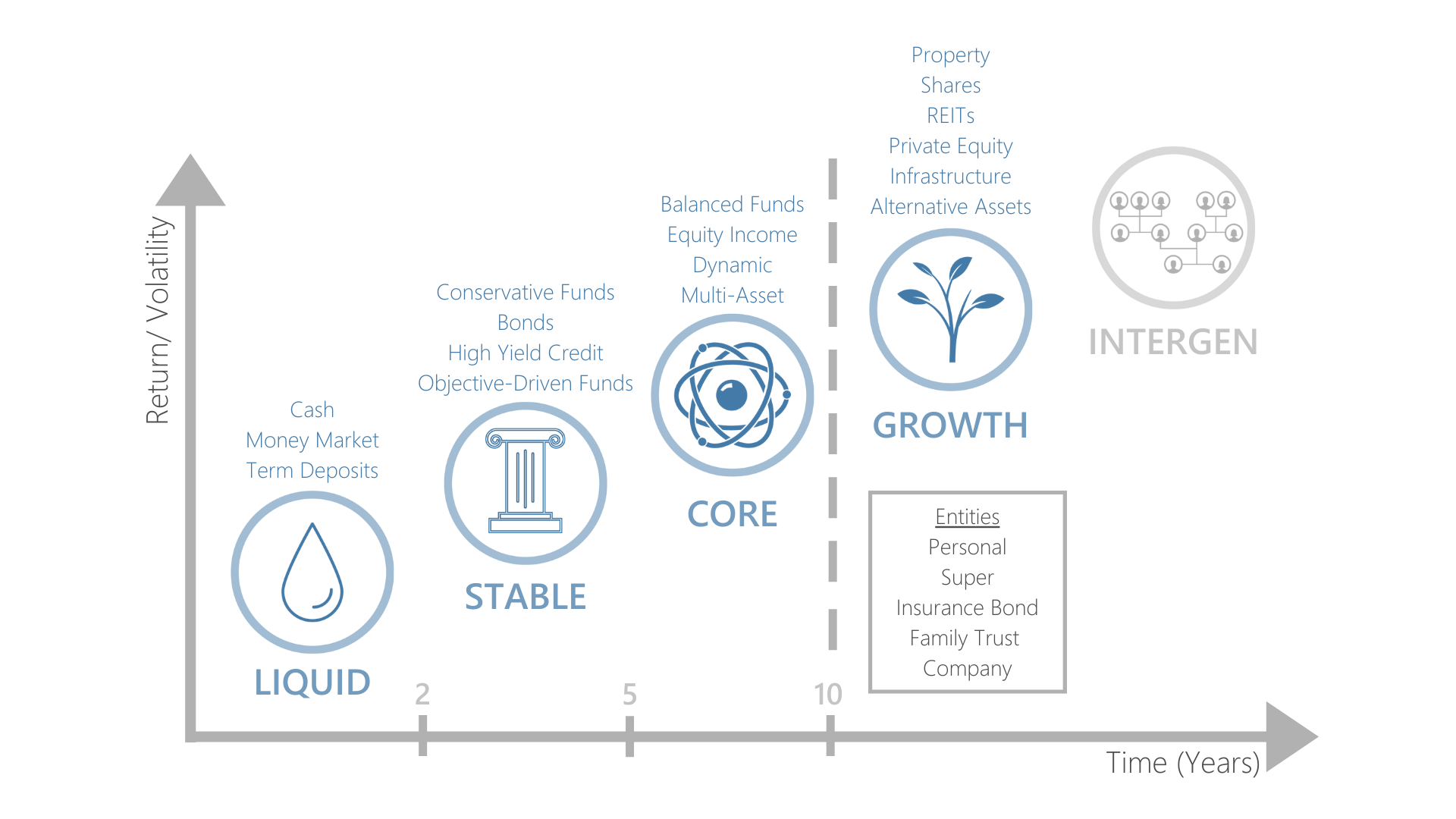

4. Employ a goals-based investment framework, matching goals and timeframes with investments

To ensure your goals are met as planned (and are not subject to how good a year your portfolio has had), an effective strategy is to construct an investment portfolio that matches your planned expenditures with appropriate investments. Set aside some of your portfolio in short-term investments to meet your short-term needs, medium-term investments to meet medium-term needs, and so on. Permanent losses occur when you sell long-term assets at depressed prices. By making sure your objectives are met without being a forced seller, your financial position will be stronger, and you will feel better, even if there has been a period of market decline. Using a goals-based investment framework reduces sequencing risk for those at or near retirement. We talk more about sequencing risk and ways to mitigate it in our Sequencing Risk whitepaper.

Figure 2: An example of a goals-based investment framework

Perhaps the most important pre-retirement strategy to put in place a few years prior to retirement is to start building (through superannuation contributions and/ or surplus cash flow) a shorter-term pool of liquid capital (or cash). This pool can be used to initially fund retirement income and other objectives, allowing the larger balance of your capital to stay invested long-term. By having cash at your disposal, you won’t be a forced seller of part of your long-term portfolio if investment markets fall.

5. Use averaging; hold cash when appropriate and average into long-term investments over time, based on the value

If, based on the evidence, markets are highly valued (or are falling), use an averaging approach to invest capital in the long-term part of your portfolio. Investing portions of your capital over time significantly reduces timing risk. Averaging is particularly relevant for those converting a defined benefit account to an accumulation account or taking large lumps of capital and topping up superannuation before establishing a superannuation pension. Of course, averaging can always be accelerated to take advantage of market declines and lower asset prices.

6. Avoid behavioural mistakes

The two main culprits for irrational – or ‘knee-jerk’ – decisions regarding money and investing are fear and greed. More recently, a new culprit has emerged: FOMO or ‘fear of missing out’, which describes social anxiety to do what others are doing. So, apart from all the other logical benefits, a goals-based approach provides a methodology to minimise irrational decision-making. On a much calmer investment journey, short-term goals are met with liquid, short-term investments, a stable pool is ready to meet medium-term objectives and to replace the liquid pool when needed, and while growth assets may fall in value, they have time to recover and play their pivotal part in generating higher long-term returns. There is no need to panic in a downturn, and life can be enjoyed without unnecessary worry.

Final thought

In the face of weakening economic conditions and investment market volatility, we believe people planning to retire should begin to act on the Six-Point Plan detailed above. Good planning, comprehensive financial modelling, and a goals-based portfolio can make a real difference to your retirement success.

If you’d like to have a chat about your situation, please contact us on (07) 3391 5055 or via email at connect@mgdwealth.com.au.

Any advice included in this communication is general and has been prepared without taking into account your objectives, financial situation or needs. As such, you should consider its appropriateness having regard to these factors before acting on it. Any tax information refers to current laws, is not based on your unique circumstances and should not be relied on as tax advice. Before you make any decision about whether to acquire a certain financial product, you should obtain and read the relevant product disclosure statement.