Federal Treasurer, Mr Josh Frydenberg, handed down the 2021/ 22 Federal Budget at 7:30 pm (AEST) on Tuesday, 11 May 2021.

A stronger than expected economic recovery from the COVID-19 recession has resulted in a budget deficit of $161 billion, $52.7 billion lower than the government’s expected deficit. With the virus still a threat to the global and domestic economy, the Budget contains various measures to support businesses and individuals with job creation, incentives, tax relief, and superannuation changes.

Existing tax reliefs, including the low and middle income tax offset, the temporary company loss carry back rules and the full expensing of depreciating assets will be extended for another 12 months. Other key changes include a modernised individual tax residency bright-line test, tax concessions for medical and biotechnology innovations and removal of the $450 threshold to be eligible for superannuation guarantee.

The full Budget papers are available at www.budget.gov.au and the Treasury ministers’ media releases are available at ministers.treasury.gov.au.

The tax highlights are set out below.

Individuals

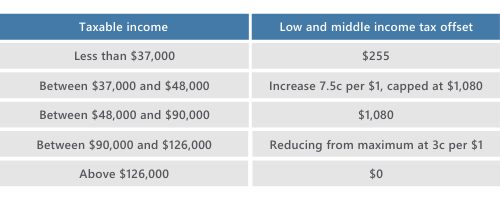

Low and middle income tax offset remains for 2021-22

The low and middle income tax offset (LMITO) will be extended for another year into 2021–22. The LMITO was due to be removed on 30 June 2021.

Consistent with the current income year, the low and middle income tax offset is calculated as follows:

Source: Budget Paper No 2, p 27.

Individual tax residency rules simplified

The individual tax residency rules will be replaced by a new framework with a primary physical presence test.

Under the new primary test, a person who is physically present in Australia for 183 days or more in any income year will be an Australian tax resident for tax purposes. Individuals who do not meet the primary test will be subject to secondary tests that consider a combination of physical presence and other measurable, objective criteria.

Currently, an individual who is physically present in Australia for 183 days or more in an income year will not be an Australian resident if their usual place of abode is overseas and they have no intention to take up residence in Australia. The new framework is based on recommendations made by the Board of Taxation in the 2019 report Reforming individual tax residency rules — a model for modernisation.

The measure will have effect from the 1 July following assent of the enabling legislation.

Source: Budget Paper No 2, p 21–22; Budget Fact Sheet “Tax incentives to support recovery”, p 8.

$250 exclusion on self-education deductions to be removed

The current limitation for individuals claiming self-education expenses, where the first $250 of the deduction is denied, will be removed. The removal of the $250 exclusion for prescribed courses of education will make it easier for individuals to work out their allowable deductions in the years they incur these expenses.

The change will come into effect from the income year following the date of assent of the relevant legislation.

There is no change to the general provisions for claiming a self-education deduction, such as requiring the expense to come from a prescribed course of education.

Source: Budget Paper No 2, p 26.

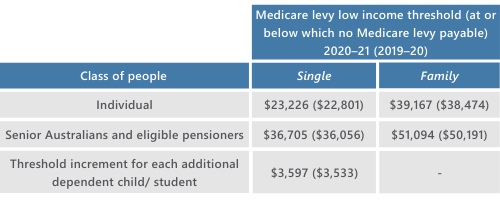

Medicare low-income thresholds for 2020-21

The CPI indexed Medicare levy low-income threshold amounts for singles, families, and seniors and pensioners for the 2020–21 year of income have been announced. The new thresholds are:

Source: Budget Paper No 2, p 24.

Full income tax exemption for ADF personnel deployed to Operation Paladin

A full income tax exemption will apply to pay and allowances of Australian Defence Force (ADF) personnel deployed to Operation Paladin from 1 July 2020. Operation Paladin includes ADF personnel deployed in Israel, Jordan, Syria, Lebanon and Egypt.

Source: Budget Paper No 2, p 24.

Home ownership funding package

The government will provide $782.1 million over 4 years from 2021–22 to increase home ownership, support jobs in the residential construction sector and enhance housing data. Funding in this package includes:

- $774.8 million over 2 years from 2021–22 for the HomeBuilder program to extend the construction commencement requirement from 6 months to 18 months for all existing applicants

- establishing the Family Home Guarantee with 10,000 places from 2021–22 to support single parents with dependants to enter, or re-enter, the housing market with a deposit of 2%

- extending the first home loan deposit scheme to provide an additional 10,000 new home guarantees in 2021–22 to allow eligible first home buyers to build a new home or purchase a newly constructed home with a deposit of 5%

- $5.8 million over 3 years from 2021–22 to continue to support the Australian Housing and Urban Research Institute to deliver the National Housing and Urban Research Program

- $1.2 million over 4 years from 2021–22 for the Australian Institute of Health and Welfare to maintain and enhance the Housing Data Dashboard website, with costs partially offset by National Housing Finance and Investment Corporation research funding.

Source: Budget Paper No 2, pp 187 and 188.

Companies and business

Extension to temporary full expensing

Temporary full expensing of eligible assets will be extended by 12 months to 30 June 2023.

Eligible businesses with aggregated turnover or income less than $5 billion will be able to deduct the full cost of eligible depreciating assets acquired from 7:30pm AEDT on 6 October 2020 and first used or installed ready for use by 30 June 2023. All other aspects of the temporary full expensing rules first introduced in the 2020–21 Budget will remain unchanged.

The temporary full expensing rules supersede the normal small business depreciation rules or depreciation under Div 40. Entities calculating depreciation under Div 40 can opt out on an asset-by-asset basis.

Normal depreciation arrangements will apply from 1 July 2023.

Source: Budget Paper No 2, p 29; Budget Fact Sheet “Tax incentives to support the recovery”, p 2.

Extension to temporary loss carry back offset

The temporary loss carry back offset will be extended by one year to apply for 2022–23 income year losses.

Eligible corporate tax entities with aggregated turnover less than $5 billion will be able to carry back losses from the 2022–23 income year to offset previously taxed profits made in or after the 2018–19 income year. The loss that can be carried back is limited by the amount of earlier taxed profits and cannot generate a franking account deficit.

Eligible companies can elect to carry back losses under this measure for any or all of the 2019–20 to 2022–23 income years.

Source: Budget Paper No 2, p 30, Budget Fact Sheet “Tax incentives to support the recovery”, p 2.

Extended powers for AAT to pause or modify ATO debt recovery

Small businesses will be able to apply to the AAT to pause or modify ATO debt recovery actions for debts being disputed in the AAT.

The Small Business Taxation Division of the Administrative Appeals Tribunal (AAT) will be allowed to pause or modify any ATO debt recovery actions, such as garnishee notices and the recovery of general interest charges or related penalties, until the underlying dispute is resolved by the AAT. The AAT will be required to ensure applications are in relation to genuine disputes and to consider the potential effect of an application on the integrity of the tax system.

The measure will apply to small business entities (including individuals carrying on a business) with an aggregated turnover of less than $10 million per year that have filed an application in relation to tax matters before the Small Business Taxation Division of the AAT.

These new powers for the AAT will be available in respect of proceedings commenced on or after the date of assent of the legislation.

Source: Budget Paper No 2, p 19; Treasurer, Minister for Employment, Workforce, Skills, Small and Family Business and Assistant Treasurer’s press release “Making it easier for small business to pause debt recovery action”, 8 May 2021.

Removing the $450 per month superannuation guarantee threshold

The employer exemption from superannuation guarantee payments for individuals earning less than $450 in salary or wages in a calendar month will be removed.

The measure will take effect from the 1 July following legislation receiving assent. The government expects to have removed this exemption category before 1 July 2022.

Source: Budget Paper No 2, p 26.

Tax-deferred employee share schemes — ceasing employment no longer a taxing point

The cessation of employment taxing point will be removed for tax-deferred employee share schemes (ESS) that are available for all companies. The change will apply to ESS interests issued from the first income year after assent of the amending legislation.

Under existing rules for a tax-deferred ESS, where certain criteria are met employees may defer tax until a later tax year (known as the deferred taxing point). By removing the cessation of employment taxing point, the deferred taxing point will be the earliest of:

- in the case of shares, when there is no risk of forfeiture and no restrictions on disposal

- in the case of options, when the employee exercises the option and there is no risk of forfeiting the resulting share and no restriction on disposal, and

- the maximum period of deferral of 15 years.

The following regulatory changes will also be made for ESS where employers do not charge or lend to employees under the ESS:

- disclosure requirements will be removed and the offer will be exempted from licensing, anti-hawking and advertising prohibitions, and

- for shares in an unlisted company, the maximum value of shares that can be issued to an employee with the simplified disclosure requirements and above exemptions will be increased from $5,000 to $30,000 per employee per year (no such value cap exists for listed companies).

The regulatory changes will apply 3 months after assent of the amending legislation.

Source: Budget Paper No 2, p 16; Budget Fact Sheet “Tax incentives to support the recovery — Supporting households, driving business investment, and creating jobs”.

Digital games tax offset to be introduced to promote growth of gaming industry

A digital games tax offset will be introduced to promote the growth of the digital games industry in Australia. This will be a refundable tax offset for a minimum investment of $500,000 from 1 July 2022 in “qualifying Australian games expenditure”.

The criteria and definition of qualifying expenditure will be determined following industry consultation. However, games with gambling elements will be excluded.

Source: Budget Paper No 2, pp 72–73; Budget Fact Sheet “Tax incentives to support the recovery — Supporting households, driving business investment, and creating jobs”.

Self-assessment of intangible depreciating assets to be allowed

Taxpayers who purchase patents, registered designs, copyrights or in-house software will be given the opportunity to self-assess their effective life for decline in value. The measure comes into effect for specified intangible assets acquired after 1 July 2023.

These assets are currently set to statutory effective life calculations. Where the taxpayer cannot reasonably estimate an effective useful life, or otherwise chooses not to self-assess, they may continue to use the statutory depreciation rates.

Source: Budget Paper No 2, p 14.

Concessional taxation of corporate income derived from certain patents

Corporate income derived from Australian medical and biotechnology patents in income years starting on or after 1 July 2022 will be taxed at a concessional effective tax rate of 17%. The mechanism by which this “patent box” concession will be delivered is subject to consultation with industry. The government intends to extend consultation in relation to the patent box with a view to determining its appropriateness for supporting the clean energy sector.

Currently, income the subject of the proposed patent box concession is undifferentiated in the income of a corporate taxpayer and accordingly subject to the rate applicable to the taxpayer, namely 25% for businesses with aggregated turnover of less than $50 million, otherwise 30%.

The patent box measure builds on the JobMaker Research and Development Tax Incentive announced in the 2020–21 Budget, by offering a competitive tax rate for profits generated from Australian owned and developed patents.

Source: Budget Paper No 2, p 23.

2021 storms and floods — income tax exemption for qualifying grants

An income tax exemption will be provided for qualifying grants made to primary producers and small businesses affected by the storms and floods in Australia.

Qualifying grants are Category D grants provided under the Disaster Recovery Funding Arrangements 2018, where those grants relate to the storms and floods in Australia that occurred due to rainfall events between 19 February 2021 and 31 March 2021.

These include small business recovery grants of up to $50,000 and primary producer recovery grants of up to $75,000. The grants will be made non-assessable non-exempt income for tax purposes.

Source: Budget Paper No 2, p 12.

ATO early engagement service for foreign investors

From 1 July 2021, a new early engagement service will be implemented to assist foreign investors and give them confidence to invest in Australian businesses. The service will:

- provide information to investors about how Australian tax laws will apply, as well as federal tax obligations

- be tailored to the particular needs of each investor

- be specific in relation to project timeframes

- integrate tax aspects of the foreign investment review board approval process, as well as assist in the time sensitive aspects of an investment transaction, and

- facilitate access to an expedited private binding rulings and advance pricing agreements where necessary.

Source: Budget Fact Sheet “Tax incentives to support the recovery — Supporting households, driving business investment, and creating jobs”.

Corporate collective investment vehicle framework revised start date

The corporate collective investment vehicles (CCIV) component of the Ten Year Enterprise Tax Plan — implementing a new suite of collective investment vehicles measure announced in the 2016–17 Budget will be finalised with a revised commencement date of 1 July 2022. The measure proposed introducing a tax and regulatory framework for CCIVs.

Source: Budget Paper No 2, p 13.

Taxation of financial arrangements — hedging and foreign exchange deregulation

Technical amendments will be made to the taxation of financial arrangements (TOFA) rules which will include facilitating access to hedging rules on a portfolio hedging basis.

The amendments aim to reduce compliance costs and correct unintended outcomes, so that taxpayers are not subject to taxation on unrealised foreign exchange gains and losses unless this is elected.

These changes will apply for relevant transactions entered into on or after 1 July 2022.

Source: Budget Paper No 2, p 29.

Junior minerals exploration incentive extended 4 more years

The junior minerals exploration incentive (JMEI) which was due to end in 2020–21 will be extended 4 more years, from 1 July 2021 to 30 June 2025.

The JMEI is a tax credit arrangement that allows junior mineral exploration companies to pass future tax deductions (losses) to Australian resident investors for greenfields mineral exploration in Australia. Minor legislative amendments will also be made to allow unused exploration credits to be redistributed a year earlier than under current settings.

Source: Budget Paper No 2, p 141; Treasurer and Minister for Resources, Water and Northern Australia’s media release “Junior miners get $100 million funding boost”, 5 May 2021.

Temporary levy on offshore petroleum production

A temporary levy will be imposed on offshore petroleum production to recover costs of decommissioning the Laminaria-Corallina oil fields and associated infrastructure. The levy will terminate on 30 June in the year in which all associated decommissioning costs have been recovered. The government will consult with industry on the proposed levy.

Source: Budget Paper No 2, p 14.

Fuel tax credits — heavy vehicle road user charge increased

The heavy vehicle road user charge will be increased from 25.8 cents per litre to 26.4 cents per litre from 1 July 2021. The charge is applied to reduce the fuel tax credit rate per litre available for vehicles with a GVM greater than 4.5 tonnes.

The increase was agreed by Commonwealth and State and Territory Transport Ministers to contribute to the construction and maintenance of roads.

Source: Budget Paper No 2, p 150.

Apprenticeship wage subsidy expanded

The Boosting Apprenticeship Commencements wage subsidy will be expanded to support businesses and Group Training Organisations that take on new apprentices and trainees.

This measure will uncap the number of eligible places (currently capped at 100,000 places). The duration of the 50% wage subsidy will be increased to 12 months from the date an apprentice or trainee commences with their employer. The subsidy will now be available from 5 October 2020 to 31 March 2022 and businesses of any size can claim the wage subsidy for new apprentices or trainees who commence during this period. Eligible businesses will be reimbursed up to 50% of an apprentice or trainee’s wages of up to $7,000 per quarter for 12 months.

Source: Budget Paper No 2, p 88.

Not-for-profits

Accessing income tax exemptions by not-for-profits

From 1 July 2023 non-charitable not-for-profits (NFPs) with active ABNs will be required to submit the information used to self-assess their eligibility for income tax exemptions in an online self-review form. This will be an annual requirement.

Currently non-charitable NFPs self-assess their eligibility for income tax exemptions, but there is no obligation to report to the ATO.

The ATO will be provided with $1.9 million capital funding to build an online system to support the measure.

Source: Budget Paper No 2, p 22.

Additions to deductible gift recipients list

The following organisations have been approved as specifically listed deductible gift recipients (DGRs) as follows:

- Australian Associated Press Ltd from 1 July 2021 to 30 June 2026

- Virtual War Memorial Limited from 1 July 2021 to 30 June 2026

- Scripture Union Queensland from 1 July 2021 to 30 June 2023

In addition, the following organisations have been approved for extension of their DGR status as follows:

- Cambridge Australia Scholarships Limited from 1 July 2021 to 30 June 2026

- Foundation 1901 Limited from 1 September 2021 to 31 August 2026

East African Fund Limited is currently operating as the School of St Jude Limited which is a public benevolent institution endorsed by the ATO as a DGR under a general DGR category. At the request of the organisation, it will be removed as a specifically listed DGR.

Gifts from $2 made to DGRs are tax deductible.

Source: Budget Paper No 2, p 25.

International tax

Changes to offshore banking unit regime

Concessional tax treatment for offshore banking units (OBUs) will be removed.

The concessional 10% effective tax rate applying to income derived from eligible offshore banking activities will be removed. Existing OBUs will have access to the concessional tax rate until the end of the 2022–23 income year. The withholding tax exemption for interest and gold fees paid by OBUs on certain offshore borrowings will be removed from 1 January 2024. The OBU regime will also be closed to new entrants from 26 October 2018.

These changes to the OBU regime have been introduced by the Treasury Laws Amendment (2021 Measures No 2) Bill 2021.

The government will consult on alternative measures to support the industry and ensure activity remains in Australia.

Source: Budget Paper No 2, p 20–21; Treasurer’s press release “Amending Australia’s Offshore Banking Unit Regime”, 12 March 2021.

List of exchange of information jurisdictions to be updated

The list of jurisdictions that have an effective information sharing agreement with Australia will be updated.

The following countries will be added to the existing jurisdictions: Armenia, Cabo Verde, Kenya, Mongolia, Montenegro and Oman.

Residents of listed jurisdictions will be eligible to access the reduced managed investment trust withholding rate of 15% on certain distributions, instead of the default rate of 30%.

The updated list will be effective from 1 January 2022.

Source: Budget Paper No 2, p 21.

NZ to maintain primary taxing right over sporting teams and support staff in Australia

The government has announced that it will ensure New Zealand maintains its primary taxing right over members of its sporting teams and support staff in respect of Australian income tax and fringe benefits tax liabilities that arise from exceeding the 183-day test in the Australia–New Zealand double tax agreement as a result of being located in Australia for league competitions because of COVID-19.

The measure will apply to the 2020–21 and 2021–22 income and fringe benefits tax years.

Source: Budget Paper No 2, pp 13 and 14.

Any advice included in this article is general and has been prepared without taking into account your objectives, financial situation or needs. As such, you should consider its appropriateness having regard to these factors before acting on it. Any tax information refers to current laws, is not based on your unique circumstances and should not be relied on as tax advice. Before you make any decision about whether to acquire a certain financial product, you should obtain and read the relevant product disclosure statement.